- 基本面量化投資:運用財務分析和量化策略獲取超額收益

- 張然 汪榮飛

- 13928字

- 2019-11-29 16:59:46

第1章 基本面量化投資綜述

1.1 導論

從《華爾街日報》到著名的金融站點thestreet.com,價值投資(或本書所稱的基本面量化投資)是當今被提及次數(shù)最多的投資戰(zhàn)略。投機者似乎可以夸耀其短期的高回報率;但在中長期,價值投資者卻遙遙領先。即使是在20世紀90年代美國股市泡沫的大崩潰中,價值投資者仍然獲得了較高的收益。那么,什么是價值投資呢?簡而言之,對上市公司股票進行比較科學的合理估值,當其市場價格低于估值時就有投資價值、就可以買進,這種投資方式就是價值投資。價值投資的基本思路如下:首先,股票市場的價格波動帶有很強的投機色彩,但是從長期看必將回歸“基本價值”,謹慎的投資者不應該追隨短期價格波動,而應該集中精力尋找價格低于基本價值的股票;其次,為了保證投資安全,最值得青睞的股票是那些被嚴重低估的股票,即市場價格明顯低于基本價值的股票,這些股票幾乎沒有下跌的空間,從谷底反彈只是時間問題,投資者集中持有這些股票就能以較小的風險獲得較大的收益。

本章主要介紹從價值投資走向基本面量化投資的思路。我們將從基于基本面的估值理論談起,回顧價值投資的理論框架,進而討論價值投資的精髓。從這些分析中可以看到,學者在學術研究中得到的有關價值投資的結論與那些傳奇的投資大師(如格雷厄姆、巴菲特和格林布拉特)所采用的投資策略其實是高度一致的。這種一致性體現(xiàn)在,業(yè)界和學界都是在深刻理解財務信息的基礎上分析股票,在構建投資策略時不僅要尋找“廉價”的股票,還要尋找“高質量”的股票。這就是價值投資的精髓。事實上,業(yè)界和學界之所以會不約而同地向同一個方向探索,是因為對于更高效地使用財務信息的追求,驅使著策略開發(fā)者想方設法地尋求更簡潔的方式處理更繁雜的信息。這就是從價值投資走向基本面量化投資的初衷,而價值投資的精髓也正是從價值投資走向基本面量化投資的思路。

本章的重點在于,基于對價值投資理論框架的回顧凝練出價值投資的精髓,并描述一些成功的、有經(jīng)驗的投資者如何利用基本面信息找到高質量的股票。另外,最近很多學術研究的成果對價值投資者尋找質量高且股價合理的股票極其有效,在后面的章節(jié)中將予以介紹。

我們先討論有效資本市場假說,進而討論噪聲投資者模型,以理解為什么市場在大部分情境下會定價錯誤;基于此,我們才能討論如何基于基本面量化投資發(fā)現(xiàn)這種定價錯誤,并為投資所用。[3]在本章末,我們還會簡要討論基本面量化投資在中國的狀況。

1.2 有效資本市場假說和噪聲投資者模型

我們想象一個最理想的證券市場,在這個市場上,證券的交易是免費的,沒有交易傭金、買賣價差(bid-ask spread)等交易成本;同時,在這個市場上也不存在證券持有成本,如賣空股票(short-sell)有關的成本。更重要的是,在這個市場上,大家擁有的信息是一樣的,對這些信息的理解也是一致且充分的。換句話說,大家對證券的估值不僅是一樣的,而且是在現(xiàn)有信息基礎上最準確的。這是一個沒有證券交易成本(trading costs)、證券持有成本(holding costs)和信息成本(information costs)的高效率市場。

可以說,有效資本市場假說(efficient market hypothesis,EMH)在一定意義上認為證券市場是一個沒有任何成本的、高效率的、理想化的市場。在有效資本市場上,證券的價格等于它的價值。一旦與證券價值相關的信息被披露,市場就會迅速做出調整,使其價格重新等于價值,沒有任何人或交易策略可以提前利用公開信息賺取超額回報。也就是說,在這個市場上,因為所有投資者擁有相同的信息,并具備相同的信息分析能力,證券的定價在任何時點上相對于投資者擁有的信息都是“對”的,錯誤定價(mispricing)是不存在的。[4]

在這種情況下,有效資本市場意味著,股票的價格在任何時點應該等于投資者在所擁有的信息的基礎上該股票預期帶來的未來各期現(xiàn)金流的折現(xiàn)值,其計算公式如下:

其中,Vt表示股票在時間t的內在價值,Et(Dt+i|δ)表示基于時間t的信息對未來第t+i期股利的預期,r表示折現(xiàn)率。公式表明在任何時間t,一只股票的價格等于其內在價值,市場是有效的。

當市場接收到關于某一公司的新信息以后,投資者根據(jù)新信息調整對未來現(xiàn)金流Et(Dt+i|δ)的預測和對折現(xiàn)率r(公司風險)的評估,股票內在價值Vt也相應發(fā)生變化。同一時間,股票價格Pt也發(fā)生同樣的變化,市場繼續(xù)保持著價格等于價值的有效狀態(tài)。

模型(1-1)從有效資本市場學派的角度對有效市場學派和行為金融學派的交鋒問題給出了回答:證券價格的決定機制是基于現(xiàn)有信息的未來現(xiàn)金流折現(xiàn),價格對信息的反應過程是及時的、充分的、完整的。

為了徹底闡明其觀點,Shiller(1984)提出一個簡單的噪聲投資者模型。該模型具有兩類投資者:精明投資者和噪聲投資者。精明投資者基于基本面信息進行交易,這些投資者能夠以無偏的行為快速回應關于基本價值的消息;相反,噪聲投資者不是依據(jù)基本面信息進行交易。這兩類投資者的具體定義如下:

精明投資者(信息投資者)

精明投資者在時間t對股票的需求Qt表示為總流通股的一部分:Qt= 。其中,Rt是在時間t股票的實際回報率,ρ是精明投資者對股票無需求時的預期實際回報,φ是精明投資者持有所有股票時的風險溢價。

。其中,Rt是在時間t股票的實際回報率,ρ是精明投資者對股票無需求時的預期實際回報,φ是精明投資者持有所有股票時的風險溢價。

噪聲投資者(普通投資者)

噪聲投資者的需求隨時間變化,且這種需求無法依據(jù)預期收益模型進行預測。他們的需求被表示為Yt(普通投資者要求的每股股票價值)。

在均衡的情形下,股票需求與股票供給等量時達到市場出清(Qt+Yt/Pt=1),求解得到的理性預期模型產生以下市場出清價格:

其中,市場價格Pt是現(xiàn)值;貼現(xiàn)率是ρ+φ,由在時間t的預期未來股息支付Et(Dt+k)加上φ乘以噪聲投資者的預期未來需求Et(Yt+k)得出。換句話說,Pt由企業(yè)的基本面價值(未來股利)和其他多變的因素(噪聲投資者未來的需求)共同決定。這兩個因素的相對重要性由φ決定,φ可以理解為套利成本。

當φ趨近于零時就出現(xiàn)一種特殊的情形,價格變成了預期股利的函數(shù)[式(1-1)],這與有效市場模型一致。因此,當市場的套利成本很低時,價格表現(xiàn)與有效市場假設的預期更加一致。然而,當φ增大時,噪聲投資者的相對重要性增大。在極端情形下,即當φ趨近于無窮大時,市場價格僅僅由噪聲投資者的需求決定,基本面估值在定價方面的作用微不足道。

什么因素影響φ呢?顯然,精明投資者的特點(如他們的風險厭惡程度和財富約束)起著重要作用。更具體而言,套利成本涉及以下方面:(1)交易成本,與建倉、平倉相關的成本,包括經(jīng)紀人傭金、價滑、買賣價差等;(2)持有成本,與持有頭寸相關的成本,受到諸如套利頭寸的持續(xù)時間和賣空成本等因素的影響;(3)信息成本,與獲得、分析和監(jiān)督信息相關的成本。

在套利成本中,最重要的因素是信息成本。估計公司價值及評估頭寸風險都要用到信息,假定有多個有經(jīng)驗的投資者,任意一個理性套利者都不能確切地了解所擁有信息的質量。請注意,φ也出現(xiàn)在式(1-2)的分母中,這意味著信息成本也會影響不同企業(yè)的估值,以及企業(yè)的資本成本(例如,投資者期望從他們對公司的投資中獲得回報)。套利成本低的市場會呈現(xiàn)價格接近基本面的情形。例如,在股票期權、指數(shù)期貨和封閉式基金的市場中,交易和信息成本呈現(xiàn)相對較低的特征。在這些市場中,估值相對直接、交易成本極低,而且交易資產往往擁有類似的替代品,因此這些資產的價格與其基本面價值緊密相聯(lián)也是預料之中的。

然而,在其他市場中,套利成本φ可能很大,因此股價由噪聲投資者支配。例如,許多新興經(jīng)濟體的資本市場具有機構投資者相對少、市場深度淺的特征,因此套利成本較高。即使在美國,一些規(guī)模較小的公司受到較少的關注、交易量較小,這類難以估值的股票(包括互聯(lián)網(wǎng)、生物技術和所謂的“基于云技術”的股票)可能會有更高的套利成本。根據(jù)噪聲投資者模型,在這些市場中,股價會呈現(xiàn)更大的波動性,并且與基本面價值的相關性較弱。

模型(1-2)表達的主要觀點是,市場價格是噪聲投資者和理性套利者在成本約束下相互作用的產物。一旦我們引入噪聲投資者和高昂的套利成本,價格就不再是基于未來預期股息的簡單函數(shù)。除非套利成本為零,否則Pt通常不等于Vt。錯誤定價的程度由噪聲投資者需求和套利成本的函數(shù)決定。換句話說,當套利成本不等于零時,我們可以預期錯誤定價是一種均衡現(xiàn)象。

從上述分析可以看出,在很多情形下,由于存在套利成本和噪聲投資者,價格不應該等于價值。這時,歷史會計信息對于公司估值和未來收益的預測就會變得特別有用,下面我們將分析成熟投資者(精明投資者)如何利用這些信息進行基本面分析或者價值投資。

1.3 基于基本面分析的量化投資

在本節(jié),我們探討如何利用歷史會計信息進行投資決策,并在這些決策思路中尋找共同點,以發(fā)現(xiàn)價值投資的精髓。我們首先討論格雷厄姆的投資方法。在基本面分析方面,本杰明·格雷厄姆(Benjamin Graham)是巴菲特、彼得·林奇等投資大師的啟蒙者。巴菲特曾虔誠地說:“在許多人的羅盤上,格雷厄姆就是到達北極的唯一指示。”大衛(wèi)·劉易斯甚至說:“格雷厄姆的《證券分析》是每一位華爾街人士的《圣經(jīng)》,格雷厄姆則是當之無愧的華爾街教父。”

1.3.1 格雷厄姆的量化投資方法

在《證券分析》最早的版本(他與戴維·多德于1934年合著)中,格雷厄姆提出了一種選股方法。格雷厄姆認為,同時擁有以下特點的股票都是值得投資的:

(1)市盈率是AAA債券收益率的2倍;

(2)股票的P/E(市盈率)不到最近5年內所有股票平均P/E的40%;

(3)股息率大于AAA公司債券收益率的2/3;

(4)價格低于有形賬面價值的2/3;

(5)價格低于凈流動資產價值(NCAV)的2/3,凈流動資產價值定義為流動資產(每股收益)減去流動負債;

(6)債務權益比率(賬面價值)必須小于1;

(7)流動資產大于2倍流動負債;

(8)負債小于2倍凈流動資產;

(9)EPS(每股收益)歷史增長(至少過去10年)大于7%;

(10)在過去10年中,盈利的下降不超兩年。

仔細觀察,你會發(fā)現(xiàn)上述十個因素可以分成兩組:比起后五個因素,前五個因素互相之間有著更加自然的聯(lián)系。前五個因素都是衡量“廉價”程度的。前兩個因素比較公司的股價與其報告的盈利,促使我們購買市盈率低于某一閾值的股票;接下來的三個因素將股票價格與其股利、賬面價值和凈流動資產價值進行比較。總體上,前五個因素告訴我們,購買那些價格相對于價值更加便宜(廉價)的公司。

后五個因素與前五個因素的不同點在于:它們不涉及股票價格。我們可以將后五個因素作為一個整體,視作對公司質量的度量,因為這些因素都是基于基本面指標的。因素(6)—(8)衡量債務(杠桿)及短期流動性(償付能力)。因素(9)和因素(10)是對公司的歷史盈利增長率和增長的一致性的度量。簡而言之,格雷厄姆想購買杠桿率低、償債能力高、一段時間內的盈利增長率表現(xiàn)不錯的公司。按照格雷厄姆的說法,高質量的公司是指那些高增長、穩(wěn)定增長、低杠桿和流動性良好的公司。

1.3.2 剩余收益模型的理論基礎

如何解釋上述現(xiàn)象呢?是否因為在回溯測試區(qū)間美國正處于一個特殊的歷史時期?為了進一步推論,我們引入基于剩余收益模型的估值理論。

剩余收益模型

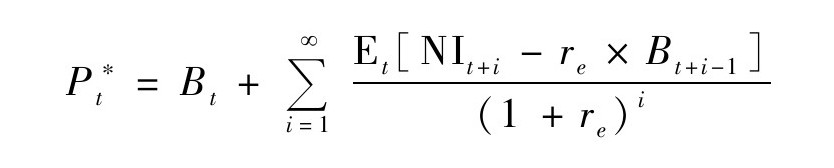

根據(jù)剩余收益模型,一家公司的價值等于其當前賬面價值和未來預期剩余收益現(xiàn)值之和,即

其中,Bt為公司在時間t的賬面價值,Et[·]為公司在時間t的期望值,NIt+i為第t+i期的凈收入,re為權益資本成本,ROEt+i為第t+i期賬面資產稅后收益率。在式(1-3)中,期間t的剩余收益(RI)定義為期間t的收益減去基于資本成本的正常收益,公式為RIt=NIt-rBt-1。

剩余收益模型使得我們可以依據(jù)企業(yè)財報數(shù)據(jù)估算公司價值(根據(jù)公司未來現(xiàn)金流計算現(xiàn)值),這也是該模型受歡迎的原因。從直覺上,我們可以把式(1-3)分解為以下形式:

其中,第t期的賬面價值為原始資本或初始投資(Capitalt),PVRIt為未來剩余收益的現(xiàn)值。式(1-4)突出公司價值(公司現(xiàn)在值多少錢)始終是兩項之和:投入資本(資產基礎)和未來剩余收益的現(xiàn)值。

事實證明,初始資本(Capitalt)對于公司價值的計算并不重要(Penman,1996,1998)。在式(1-4)中使用現(xiàn)在的賬面價值作為初始投資,但是我們可以選擇幾乎任何數(shù)值作為起始資本。

隨后的研究提出除賬面價值外,還可以用其他的替代指標作為初始資本。例如,資本化的1年盈利預測或當年的銷售收入。剩余收益模型告訴我們,對于每個選定的初始資本,我們可以計算與其匹配的PVRIt(等于未來支付給股東的現(xiàn)值)。

剩余收益模型如何幫助我們進行基本面分析?它讓我們更清楚地看到能夠推動股價倍增的績效指標。例如,將式(1-3)兩邊除以公司的賬面價值,我們可以根據(jù)預期凈資產收益率重新表達價格賬面比(市凈率)。

其中,Pt為公司在時間t的預期股利的現(xiàn)值,Bt為公司在時間t的賬面價值,Et[·]為在時間t的期望值,re為權益資本成本,ROEt+i為第t+i期的稅后賬面收益率。

式(1-5)表明,一家公司的市凈率是由預期ROE、資本成本(re)及其未來的賬面價值增長率(取決于未來ROE和股息支付率k)的函數(shù)決定的。那些有著類似市凈率的公司的未來剩余收益現(xiàn)值[式(1-3)右邊的無限求和]也是相似的。

同樣,我們可以得出企業(yè)價值與銷售比(EV/S)。根據(jù)Bhojraj and Lee(2002),如果我們模擬企業(yè)在初始期間(假設n年)高增長,后續(xù)為更穩(wěn)定的永續(xù)增長期,企業(yè)的EV/S可以表示如下:

其中,EV*t為在時間t的總企業(yè)價值(債務加權益),St為在時間t的總銷售額,Et[·]為基于在時間t可用信息的期望值,PM為營業(yè)利潤率,k為恒定支付比率,r為資本成本,g1為初始盈利增長率(適用于n年),g2為n+1年以后的永續(xù)增長率。

式(1-6)表明,企業(yè)的EV/S是預期營業(yè)利潤率(PM)、支付比率(k)、預期增長率(g1和g2)和資本成本(re)的函數(shù)。這有助于我們回答以下問題:哪些公司值得更高的EV/S?答案是,那些具有較高預期利潤率、較快增長率、較高支付比率和較低資本成本的公司。

1.3.3 價值投資的兩個關鍵要素

剩余收益模型框架將企業(yè)價值分解為兩個關鍵要素——投入資本與未來剩余收益的現(xiàn)值(增長機會),從而使企業(yè)價值變得易于計算。典型廉價指標的一個很大問題在于,它們只比較股票的價格與其投入資本(賬面價值),而完全忽略了股票估值的第二個要素——增長機會。

從格雷厄姆開始,最成功的基本面投資者始終把價值投資視為兩個關鍵要素的組合——尋找質量好的公司和以“合理的價格”買入,可以用下式表示:

價值投資=廉價+質量(1-7)

企業(yè)的市盈率是對現(xiàn)有資產是否便宜的衡量標準,這是價值投資比較容易但不太有趣的部分;有趣的部分要求投資者評估企業(yè)的質量,使用當前可用的各種衡量指標預測未來剩余收益的現(xiàn)值(PVRI)。這就是我們所說的基本面分析的核心部分。最好的基本面投資者專注于購買“廉價”且優(yōu)質的股票,格雷厄姆正是基于這種邏輯構建了選股法。回到格雷厄姆的企業(yè)質量因素[因素(6)到因素(10)],他基于此建立了原始股票池。格雷厄姆直觀地認識到,擁有較低杠桿、較高流動性和較高穩(wěn)定增長率的企業(yè)在未來最有可能產生高回報率,或者說在剩余收益模型的框架下,他認為具有這些特征的是高PVRI股票。

1.3.4 業(yè)界的實踐

如果想了解如巴菲特、芒格、格林布拉特等投資大師的投資方法,甚至想了解一些著名的基金的投資策略,那么時刻牢記“廉價+質量”的投資原則是非常重要的。下面我們以格林布拉特及其神奇公式作為例子,詳細講解這一原則的應用。

格林布拉特和神奇公式

格林布拉特是美國學者,同時也是對沖基金經(jīng)理、投資者和作家。與格雷厄姆一樣,格林布拉特的職業(yè)跨越了學術界和華爾街。1985年,他成立了一家對沖基金——戈坦資本(Gotham Capital),專注于特殊事件類投資。戈坦資本在1985年成立之后的10年間,扣除管理費前的資產以年40%的驚人速度增長。在1995年返還所有的外部資本之后,格林布拉特和聯(lián)合創(chuàng)始人以自有資金繼續(xù)進行特殊事件類投資。1999年,格林布拉特出版了他的第一本暢銷書——《股市天才》[6],描述了戈坦資本是如何取得成功的。

不過,格林布拉特最出名的是他的第二本書《股市穩(wěn)賺》[7],這本書也在市場上大賣。該書于2005年首版,銷量超過30萬冊,被翻譯成16種語言。在格林布拉特看來,這本書是探討巴菲特的投資策略能否量化的實驗產物。他知道“來自奧馬哈的圣人”可能無法被量化;不過,他還是想知道那些巴菲特的魔法能否被模仿。

大多數(shù)人是通過巴菲特在伯克希爾-哈撒韋(Berkshire Hathaway)公司的“董事長致辭”學習其投資理念的,而格林布拉特則發(fā)現(xiàn)了一個可以量化的公式。正如巴菲特經(jīng)常說的那樣,“以平常的價格買進一家非凡的公司遠遠勝過以非凡的價格買進一家平常的公司”。格林布拉特觀察到,巴菲特購買的不是廉價的公司,而是價格合理的優(yōu)質公司。如果我們試圖創(chuàng)建一個量化選股法以合理的價格購買非常棒的公司,那么會發(fā)生什么呢?

在《股市穩(wěn)賺》一書中,格林布拉特提出了神奇公式,這其實是一種非常簡單的策略。格林布拉特基于兩個因素對公司進行排名:資本回報率(return on capital,ROC)和盈利收益率(earning yield,EY)。[8]神奇公式,簡而言之,就是尋找那些擁有較高歷史資本回報率(過去5年內,年資本回報率至少20%),并且當前以較高盈利收益率交易的公司。

我們應注意以下兩點:第一,神奇公式是可以賺取超額收益的(更準確地說,它在很長的一段時間里可以賺取超額收益),這個公式已經(jīng)由格林布拉特和其他人使用美國數(shù)據(jù)進行了回溯測試,排在選股法頂部的公司在過去五十多年的表現(xiàn)大幅超過平均水平;第二,這與格雷厄姆在過去很多年里所做的事情相似,即五年持續(xù)高增長、低P/E等。

回到剩余收益模型公式,我們發(fā)現(xiàn)格雷厄姆、巴菲特和格林布拉特都在做同樣的一件事:找到高PVRI預期的公司,在合理的P/E水平上交易。巴菲特最常見的原則如下:(1)只投資你所熟悉業(yè)務的公司;(2)尋找具有可持續(xù)競爭優(yōu)勢的公司;(3)擁有高質量管理團隊的公司;(4)購買具有良好的“安全邊際”的公司。最后一項原則是最容易理解和實現(xiàn)的——購買相對于其資本金基礎更有吸引力估值的公司。前三項原則告訴我們什么呢?他們是否并不只是將我們指向未來更可能具有高可持續(xù)ROE(凈資產收益率)的公司?答案顯而易見:質量很重要。

1.3.5 學術界的證據(jù)

我們已經(jīng)討論了基于基本面估值的基本框架,學術界近年來的實證研究結果也證實了采用上文討論的方法能獲得超額收益,下面我們具體介紹實證研究結果。

廉價

會計學和金融學領域的大量文獻證明了價值效應,即價值股(股票價格低于它們的基本面價格)勝過魅力股(股票價格高于它們的基本面價格)的趨勢。常用的價值衡量指標是市賬比率(Stattman,1980;Rosenberg et al.,1985;Fama and French,1992)、盈利價格比(Basu,1977;Reinganum,1981)、現(xiàn)金流與價格比(Lakonishok et al.,1994;Desai et al.,2004)和銷售額與企業(yè)價值之比(O’Shaughnessy,2011)。價值溢價的效果隨時間而變化,但價值股的回報高于魅力股的基本結論在學術文獻中是非常穩(wěn)健的。

雖然學者普遍接受實證結果,但是對于其背后的原因卻沒有達成共識。有人認為實證結果清楚地表明了價值股的價格被低估(“便宜貨”);有人則認為價格便宜只是一方面原因,另外一方面原因是衡量價值的常見指標也意味著某種風險。例如,F(xiàn)ama and French(1992)認為,低P/B(市凈率)的股票面臨更多的風險;Zhang(2005)認為,這些股票包含更多的“被困資產”[9],因此更容易受到經(jīng)濟下滑的影響。

質量

到目前為止,學術界關于高質量公司的定義(或特征)尚未達成共識。例如,許多論文檢驗了盈余持續(xù)性或其他會計指標預測未來回報的能力,但大多數(shù)論文沒有在企業(yè)質量的框架下討論這個主題。當把這些零散的實證發(fā)現(xiàn)拼湊起來時,我們就會發(fā)現(xiàn)得到的結論與格雷厄姆選股法所定義的質量維度非常相似,這些實證結論也與我們的估值理論框架非常吻合。

決定一家公司未來剩余收益現(xiàn)值(PVRI)的關鍵是什么?最重要的是影響公司未來盈利能力和增長的因素,它們是公司未來凈資產收益率的主要驅動力。公司資產是否安全也十分重要。安全公司的資本成本(re)更低,在未來預期現(xiàn)金流量一定的情況下,安全公司將得到更高的PVRI。最后,預期的派息率也很重要。在盈利能力和增長率相同的情況下,給投資者派息更多的公司擁有更高的PVRI。

實證研究和業(yè)界實踐在上述幾個方面得出的結論是一致的。如果一家公司穩(wěn)定、安全、盈利能力強且增長穩(wěn)定,同時其現(xiàn)金流狀況良好、派息率高,那么這家公司未來越有可能獲得高投資回報率。

盈利能力和增長

盈余質量

不僅盈余的數(shù)量很重要,盈余的質量(如可持續(xù)性)也很重要。例如,Sloan(1996)和Richardson et al.(2005)的研究表明,盈余的現(xiàn)金流部分比應計部分更具有持續(xù)性。Novy-Marx(2013)的研究表明,毛利(銷售收入-銷售成本)是比凈利潤更好的衡量盈利能力的指標。他們的實證結果表明,盡管高盈利公司的估值倍數(shù)顯著高于低盈利公司,但是高盈利公司的回報率仍然高于低盈利公司。

盈余質量的另一個研究領域探討了如何使用會計數(shù)據(jù)識別財務造假。Beneish(1999)基于財務報表數(shù)字,提出一個可識別盈余操縱的打分模型——M-score。在樣本外測試中,Beneish et al.(2013)的研究表明,M-score可以正確識別盈余操縱公司,71%的會計欺詐案件在被公開披露之前可以通過M-score得以識別。同時,他們的研究也表明,M-score是股票收益率的強大預測工具,在控制其他因素(包括會計應計利潤)后,M-score高的公司(盈余操縱可能性更大的公司)的股票未來收益率低。

總體而言,這些研究表明,相比凈利潤,基于現(xiàn)金流或毛利衡量的盈利能力能夠更好地預測未來股票回報。

安全性

學術界的研究基于不同衡量公司安全的指標都得出了同樣的結論:股票越安全,股票回報率越高。例如,低波動率公司(Falkenstein,2012;Ang et al.,2006)、低貝塔值公司(Black et al.,1972;Frazzini and Pedersen,2014)、低杠桿公司(George and Hwang,2010;Penman et al.,2007)、低財務風險公司(Altman,1968;Ohlson,1980;Dichev,1998;Campbell et al.,2008)的股票回報率更高。

換句話說,具有較高波動率、較高貝塔值、較高杠桿和更高破產風險的公司,其股票回報率較低。然而這些發(fā)現(xiàn)在均衡資產定價框架下是講不通的。在均衡條件下,具有較高風險的公司應該有更高的未來回報。但是,如果我們相信這些風險度量與計算公司PVRI的貼現(xiàn)率相關,那么就說得通了。因為“更安全”的公司具有更低的資本成本(re),在其他條件相同的情況下,“更安全”公司的PVRI高于“風險較大”公司的PVRI。如果市場低估了公司的真實PVRI,那么“更安全”公司實際上實現(xiàn)了更高的未來回報。

股息率

最后,向股東(債權人)支付更高股息(利息)的公司,其股票回報率也更高。例如,回購股票的公司往往表現(xiàn)良好(Baker and Wurgler,2002;Pontiff and Woodgate,2008;McLean et al.,2009),而發(fā)行更多股票的公司往往表現(xiàn)更糟糕(Loughran and Ritter,1995;Spiess and Affleck-Graves,1995)。債券市場也類似。發(fā)行更多債務的公司,其超常收益為負(Spiess and Affleck-Graves,1999;Billett et al.,2006);而清償債務的公司,其超常收益為正(Affleck-Graves and Miller,2003)。Bradshaw et al.(2006)的研究表明,可以根據(jù)公司的現(xiàn)金流量表,計算外部融資活動凈額指標衡量這些影響。總體而言,這些發(fā)現(xiàn)與剩余收益模型框架是一致的:較高資本回報率的公司(具有更高的k)擁有更高的PVRI。

那么,什么類型的公司可以被視為高質量的?換言之,什么公司特征與未來更高的ROE、更低的資本成本及更高的派息率相關呢?現(xiàn)有的學術研究表明,那些安全、盈利的成長型公司能給投資者帶來更高的回報。如果市場低估了其基本面價值,那么高質量的公司就可以賺取更高的未來回報。這種現(xiàn)象很難歸因于價值效應是一種風險,因為高質量公司的盈利能力更強、更穩(wěn)定、更不容易陷入困境,并擁有更持久的未來現(xiàn)金流和較低的經(jīng)營杠桿。

在一項最新的研究中,Asness et al.(2014)將不同的質量因子放在一起研究。在這項研究中,他們定義高質量公司為“安全、可盈利、有成長性和經(jīng)營良好”的。他們認為在其他條件相同的情況下,投資者愿意向這樣的公司投入更多的資金,這表明市場實際上沒有為這些優(yōu)質股票支付足夠高的溢價。他們在質量維度上對公司進行排序,構造了QMJ(quality minus junk)投資組合,發(fā)現(xiàn)投資組合在23個國家中的22個國家獲得了正的超額回報。

盈利性指標

盈利性指標包含六個變量,衡量了投資回報率(ROA、ROE)、毛利(GPOA、GMAR)[10]、經(jīng)營性現(xiàn)金流(CFOA、ACC)[11]。分子分別是當年的收入、毛利或者經(jīng)營性現(xiàn)金流;分母分別是總資產、權益面值、總銷售額或者利潤。上述指標值越大,說明公司的盈利性越好。

成長性指標

成長性指標度量公司過去五年的盈利變化,包含多個變量。例如,ΔGPOA=(GPt-GPt-5)/TAt-5,其中GP=RE-COGS,TA是總資產。換言之,Asness et al.(2014)將成長性公司定義為毛利、收入或者現(xiàn)金流在過去五年里持續(xù)增長的公司。上述指標值越大,說明公司的成長性越好。

安全性指標

安全性指標包含六個變量,分別為貝塔值、股價波動性(IVOL)[12]、盈利波動性(EVOL)[13]、杠桿率(LEV)[14]及財務風險(O-score、Z-score)[15]。上述指標值越小,說明公司的安全性越高。

派息率指標

派息率指標包含三個變量,分別為凈股票發(fā)行量(EISS)[16]、凈債務發(fā)行量(DISS)[17]、股利支付率(NPOP)[18]。前兩個變量值越大,說明公司派息率越低;股利支付率越高,說明派息率越高。

上述指標的構建與剩余收益模型框架是契合的,盈利性指標關注的是公司的盈利性,成長性指標關注的是盈利能力的成長性。在剩余收益模型框架中,這21個變量與未來ROE相關;而Asness et al.(2014)的研究也發(fā)現(xiàn)這些指標與P/B高度相關。

1.4 量化投資在中國:機遇和挑戰(zhàn)并存

關于量化投資在中國的適用性問題,我們的基本看法是,量化投資尤其是基于基本面的量化投資,在中國既存在機遇也存在不少挑戰(zhàn)。

就機遇方面而言,由于中國A股市場目前仍然是散戶居多,存在大量的噪聲投資者,這些噪聲投資者的存在使得市場處于較長期的無效狀態(tài),價格修正要比在成熟市場花更長的時間,這時基本面量化投資者或價值投資者就可以利用這個機會,開發(fā)基于價值的投資模型,從市場獲利。事實上,量化投資在中國正處于蓬勃發(fā)展期。截至2016年第三季度,A股市場量化對沖產品的規(guī)模已超過2 500億元,在普通權益投資中占比8.4%(2012年占比為2.2%)。可以看出,量化產品占比逐年上升,但仍處于較低的水平,未來仍有很大的發(fā)展空間。[19]

就挑戰(zhàn)方面而言,第一,由于中國資本市場的機構投資者相對較少、市場深度較淺,因此套利成本較高。在這種情況下,股票價值和基本面的相關性與發(fā)達市場相比較低,從而制約了價值投資者的獲利空間。第二,基本面量化采用的交易策略是分析研究歷史數(shù)據(jù)得到的,是對歷史規(guī)律的總結,其基本假設為之前的規(guī)則在未來是不變的,因此可以通過相同的方法在未來獲取超額收益。但這種假設在新興資本市場時常會受到?jīng)_擊,政策變化、交易規(guī)則變動都可能破壞之前的規(guī)則,這時采用量化投資方法的投資者就會感到無所適從。第三,在新興資本市場,量化和對沖工具相對缺乏或者成本很高,使得價格長期無法回歸價值,這對量化投資者的挑戰(zhàn)性更大。

總而言之,中國資本市場既存在顯著的套利機會,也存在顯著的套利成本。我們相信,隨著中國資本市場的逐步完善,套利成本會逐漸減少,量化投資者對套利機會的捕捉使得市場更有效率,而基于基本面的量化投資也將在中國得到越來越廣泛的應用。

本章小結

本章主要介紹從價值投資走向基本面量化投資的思路。噪聲投資者模型表明,股票市場中由于存在套利成本和噪聲投資者,“沒有免費的午餐”并不等于“價格正確”。面對錯誤定價帶來的投資機會,學界和業(yè)界的分析思路高度一致:尋找“廉價”且高質量的股票——這就是價值投資的精髓。價值投資離不開基本面分析,而對更高效地使用基本面信息的追求,驅使著投資策略開發(fā)者尋求更簡潔的方式處理更繁雜的信息——這就是從價值投資走向基本面量化投資的初衷。

思考與討論

思考與討論參考答案

參考文獻

[1]Affleck-Graves,J.and R.E.Miller,2003,The information contentof calls of debt:Evidence from long-run stock returns,Journal of Financial Research,26(26):421—447.

[2]Altman,E.I.,1968,F(xiàn)inancial ratio,discriminant analysis and the prediction of corpo-rate bankruptcy,Journal of Finance,23(4):589—609.

[3]Ang,A.,R.J.Hodrick,Y.Xing and X.Zhang,2006,The cross-section of volatility and expected returns,The Journal of Finance,61(1):259—299.

[4]Asness,C.S.,A.Frazzini and L.H.Pedersen,2014,Quality minus junk,Working Paper,AQR Capital Management and New York University.

[5]Baker,M.and J.Wurgler,2002,Market timing and capital structure,Journal of Fi-nance,57(1):1—32.

[6]Basu,S.,1977,The investment performance of common stocks in relation to their price-to-earnings:A test of the efficient markets hypothesis,Journal of Finance,32(3):663—682.

[7]Beneish,D.,C.M.C.Lee and C.Nichols,2013,Earnings manipulation and expec-ted returns,Financial Analysts Journal,69(2):57—82.

[8]Beneish,D.,1999,The detection of earnings manipulation,Financial Analysts Jour-nal,55(5):24—36.

[9]Bhojraj,S.and C.M.C.Lee,2002,Who is my peer?A valuation-based approach to the selection of comparable firms,Journal of Accounting Research,40(2):407—439.

[10]Billett,M.T.,M.J.Flannery and J.A.Garfinkel,2006,Are bank loans special?Evidence on the post-announcement performance of bank borrowers,Journal of Financial and Quantitative Analysis,41(4):733—751.

[11]Black,F.,M.C.Jensen and M.Scholes,1972,The capital asset pricing model:Some empirical tests,in Jensen,M.C.,Studies in the Theory of Capital Markets,New York:Praeger,pp.79—121.

[12]Bradshaw,M.,S.Richardson and R.Sloan,2006,The relation between corporate financing activities:Analysts'forecasts and stock returns,Journal of Accounting and Economics,42(1—2):53—85.

[13]Campbell,J.,J.Hilscher and J.Szilagyi,2008,In search of distress risk,Journal of Finance,63(6):2899—2939.

[14]Dechow,P.M.,R.G.Sloan and A.P.Sweeney,1996,Causes and consequences of earnings manipulation:An analysis of firms subject to enforcement actions by the SEC,Contempo-rary Accounting Research,13(1):1—36.

[15]Desai,H.,S.Rajgopal and M.Venkatachalam,2004,Value-glamour and accruals mispricing:One anomaly or two?The Accounting Review,79(2):355—385.

[16]Dichev,I.,1998,Is the risk of bankruptcy a systematic risk?Journal of Finance,53(3):1131—1147.

[17]Falkenstein,E.G.,2012,The Missing Risk Premium:Why Low Volatility Investing Works,Create Space Independent Publishing Platform.

[18]Fama,E.,1991,Efficient capital markets:II,Journal of Finance,46(5):1575—1617.

[19]Fama,E.F.and K.R.French,1992,The cross-section of expected stock returns,Journal of Finance,47(2):427—465.

[20]Frankel,R.and C.M.C.Lee,1998,Accounting valuation,market expectation,and cross-sectional stock returns,Journal of Accounting and Economics,25(3):283—319.

[21]Frazzini,A.and L.H.Pedersen,2014,Betting against beta,Journal of Financial E-conomics,111(1):1—25.

[22]George,T.J.and C.Y.Hwang,2010,A resolution of the distress risk and leverage puzzles in the cross section of stock returns,Journal of Financial Economics,96(1):56—79.

[23]Greenblatt,J.,2010,The Little Book That still Beats the Market,Hoboken,NJ:John Wiley and Sons.

[24]Lakonishok,J.,A.Shleifer and R.W.Vishny,1994,Contrarian investment,extrap-olation,and risk,Journal of Finance,49(5):1541—1578.

[25]Lee,C.M.C.,2014,Value investing:Bridging theory and practice,China Account-ing&Finance Review,16(2):1—29.

[26]Loughran,T.and J.Ritter,1995,The new issues puzzle,Journal of Finance,50(1):23—51.

[27]Malkiel,B.G.and E.F.Fama,1970,Efficient capital markets:A review of theory and empirical work,Journal of Finance,25(2):383—417.

[28]McLean,D.,J.Pontiff and A.Watanabe,2009,Share issuance and cross-sectional returns:International evidence,Journal of Financial Economics,94(1):1—17.

[29]Mohanram,P.S.,2005,Separating winners from losers among low book-to-market stocks using financial statement analysis,Review of Accounting Studies,10(2):133—170.

[30]Novy-Marx,R.,2013,The other side of value:The gross profitability premium,Jour-nal of Financial Economics,108(1):1—28.

[31]Ohlson,J.A.,1980,F(xiàn)inancial ratios and the probabilistic prediction of bankruptcy,Journal of Accounting Research,18(1):109—131.

[32]O'Shaughnessy,J.P.,2011,What Works on Wall Street,Fourth Edition,McGraw-Hill.

[33]Penman,S.H.,1998,A synthesis of equity valuation techniques and the terminal value calculation for the dividend discount model,Review of Accounting Studies,2(4):303—323.

[34]Penman,S.H.,S.Richardson and I.Tuna,2007,The book-to-price effect in stock returns:Accounting for leverage,Journal of Accounting Research,45(2):427—467.

[35]Penman,S.H.,1996,The articulation of price-earnings ratios and market-to-book ra-tios and the evaluation of growth,Journal of Accounting Research,34(2):235—259.

[36]Piotroski,J.and E.So,2013,Identifying expectation errors in value/glamour strate-gies:A fundamental analysis approach,Review of Financial Studies,25(9):2841—2875.

[37]Piotroski,J.,2000,Value investing:The use of historical financial statement infor-mation to separate winners from losers,Journal of Accounting Research,38(Supplement):1—41.

[38]Pontiff,J.and W.Woodgate,2008,Share issuance and cross-sectional returns,Journal of Finance,63(2):921—945.

[39]Reinganum,M.R.,1981,Misspecification of capital asset pricing:Empirical anomalies based on earnings'yield and market values,Journal of Financial Economics,9(1):19—46.

[40]Richardson,S.,R.G.Sloan,M.Soliman and I.Tuna,2005,Accrual reliability,earnings persistence,and stock prices,Journal of Accounting and Economics,39(3):437—485.

[41]Rosenberg,B.,K.Reid and R.Lanstein,1985,Persuasive evidence of market inef-ficiency,Journal of Portfolio Management,11(3):9—17.

[42]Shiller,R.J.,1981,Do stock prices move too much to be justified by subsequent changes in dividends?American Economic Review,71(3):421—436.

[43]Shiller,R.J.,1984,Stock prices and social dynamics,The Brookings Papers on Economic Activity,2:457—510.

[44]Sloan,R.G.,1996,Do stock prices fully reflect information in accruals and cash flows about future earnings?The Accounting Review,71(3):289—315.

[45]Spiess,K.and J.Affleck-Graves,1999,The long-run performance of stock returns following debt offerings,Journal of Financial Economics,54(1):45—73.

[46]Spiess,K.and J.Affleck-Graves,1995,Underperformance in long-run stock returns following seasoned equity offerings,Journal of Financial Economics,38(3):243—267.

[47]Stattman,D.,1980,Book values and stock returns,The Chicago MBA:A Journal of Selected Papers,4:25—45.

[48]Zhang,L.,2005,The value premium,Journal of Finance,60(1):67—103.